The USDA made only minor changes to their domestic supply demand tables this month. The USDA corn and soybean yield estimates didn’t change this month. Neither did the domestic carryout estimate for soybeans. The corn ending stocks estimate came in 83 million smaller than the average trade estimate, which makes the report lean positively for corn. Domestic wheat ending stocks were smaller but didn’t fall quite as much as trade expected.

Fifteen minutes after the reports, markets are all trading nearly exactly where they were heading into the report release. This suggests it was a sleeper of a report and traders have already moved on and are likely more focused on pending weather forecasts than the tweaks to the USDA fundamentals.

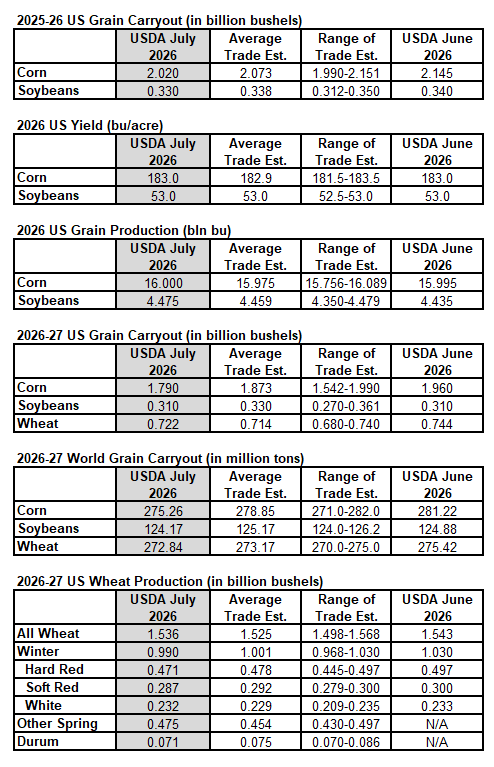

USDA – CORN

This month’s 2026/27 U.S. corn outlook is for smaller supplies, greater exports, and reduced ending stocks.

Corn beginning stocks are cut 125 million bushels to 2.0 billion, reflecting an increase in feed and residual use that is partly offset by a reduction in corn used for ethanol for 2025/26. Feed and residual use is raised 150 million bushels based on indicated disappearance in the June 30 Grain Stocks report.

Corn production for 2026/27 is up fractionally based on updated planted and harvested area from the June 30 Acreage report. The yield is unchanged at 183.0 bushels per acre. Total use is raised 50 million bushels on an increase in exports. Exports are higher reflecting expectations of continued global demand strength. With use rising and supply falling, ending stocks are down 170 million bushels to 1.8 billion. The season-average farm price received by producers is unchanged at $4.40 per bushel.

Notably, the USDA bumped their Argentine corn production estimate up another 2 million tons to 63.0 million tons.

USDA – SOYBEANS

The soybean yield forecast is unchanged at 53.0 bushels per acre. Soybean supplies for 2026/27 are raised 30 million bushels as higher production is partly offset by lower beginning stocks. Soybean crush remains unchanged for both 2025/26 and 2026/27 with offsetting changes in soybean meal demand, reflecting higher exports and lower domestic consumption. Soybean exports are raised 30 million bushels on increased supplies and stronger global demand.

Higher supplies are offset by higher use, leaving ending stocks unchanged at 310 million bushels for 2026/27. Prices are unchanged for 2026/27. The U.S. season-average soybean price is forecast at $11.40 per bushel;

USDA – WHEAT

The outlook for 2026/27 U.S. wheat this month is for lower supplies, unchanged domestic use and exports, and smaller ending stocks. Supplies are reduced 22 million bushels on lower beginning stocks and production. Production is forecast at 1,536 million bushels, down 7 million from last month.

This is the lowest U.S. wheat production since 1970/71.

The all wheat yield is 47.9 bushels per acre, up 0.9 bushels from last month. Winter wheat production is lowered 39 million bushels to 990 million, almost entirely due to reductions in Hard Red Winter and Soft Red Winter.

The initial 2026/27 survey-based production forecasts from NASS indicate other spring wheat is less than last year at 475 million bushels on lower harvested area while Durum is also lower at 71 million on reduced harvested area and yields. Projected 2026/27 ending stocks are reduced 22 million bushels to 722 million and are down 22 percent from last year. The projected 2026/27 season average farm price (SAFP) is unchanged at $6.00 per bushel, compared to last year’s final SAFP of $5.06.

Source: USDA, Reuters