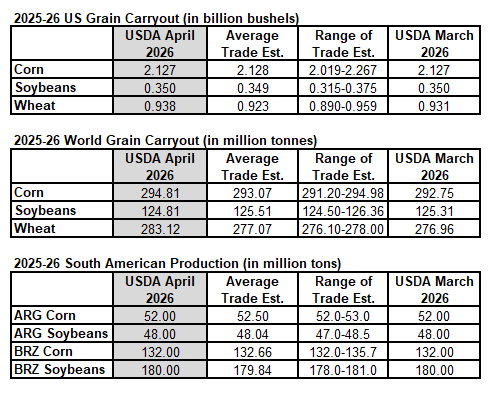

As is often the case, the April WADE report was an overall sleeper. The USDA made few substantial changes to their supply demand numbers this month. Instead, they chose to kick the can down the road to the May reports, which are typically more closely watched because it includes their initial 2026-27 crop year estimates.

First off, US carryout for corn and soybeans was unchanged. They made no changes to the US corn balance sheet while they offset a 35 million bushel increase to crush with a 35 million bushel decrease to exports. Only minor tweaks were made to the domestic wheat balance sheet, which increased ending stocks by a negligible 7 million bushels.

The global balance sheets contained larger, but not hugely significant changes. World corn ending stocks were larger month to month as expected but came in at the top end of the trade range, exceeding the average trade estimate by 1.74 million tons. While it is a shift towards larger global corn ending stocks, the difference is only about 0.6% above average trade expectations.

Global soybean ending stocks came in a little smaller than trade expectations, toward the lower side of the trade range.

The global wheat balance sheet saw the largest relative change, as ending stocks increased 6 million tons, which exceeded the high end of the trade range by 5 million metric tons. Global wheat supplies increased, with production increases largely attributed to the EU and Russia. Consumption was lowered by 4.7 million tons. Year to year, global wheat ending stocks are 24 million tons (+9%) larger than last year.

Thirty minutes after the reports, corn was trading -4 cents lower, soybeans +2 cents higher, and wheat about -10cents lower. We will likely have wheat Buy Signals beginning tomorrow.

The USDA left their South American production estimates unchanged this month.

Source: USDA, Reuters